Profit from stock market trading is considered official income, and investors are required to pay a 13% personal income tax (NDFL). However, there are ways to reduce the tax rate or even avoid paying it altogether.

Contents

- Investing in Securities for a Three-Year Period

- Investing in Securities of High-Tech Companies for One Year

- Purchasing Securities on an Individual Investment Account (IIA)

- Tax Benefits for IIA-3

- Purchasing Coupon-Bearing Bonds

- Using Losses to Offset Taxes

- Purchasing Ministry of Finance Eurobonds

Investing in Securities for a Three-Year Period

Long-term investors can take advantage of a tax benefit and be exempt from paying NDFL on profits from selling securities. However, this benefit applies only under certain conditions:

- Securities must be continuously owned by the investor for at least three years;

- The maximum profit amount that is exempt from tax is calculated using the formula: 3 million rubles for each full year of ownership (for example, if you own securities for three years, up to 9 million rubles in profit is exempt);

- The benefit applies to securities (stocks, bonds, shares of mutual funds) traded on Russian stock exchanges, such as the Moscow Exchange;

- The tax benefit is available only to tax residents of the Russian Federation;

- The tax benefit applies exclusively to profits from selling securities and does not cover dividends on stocks or coupon payments on bonds.

To claim the benefit, investors should contact their stock broker (management company), which will assist with the process. If the investor continues to hold the securities after the three-year period, the benefit can be extended for each subsequent year.

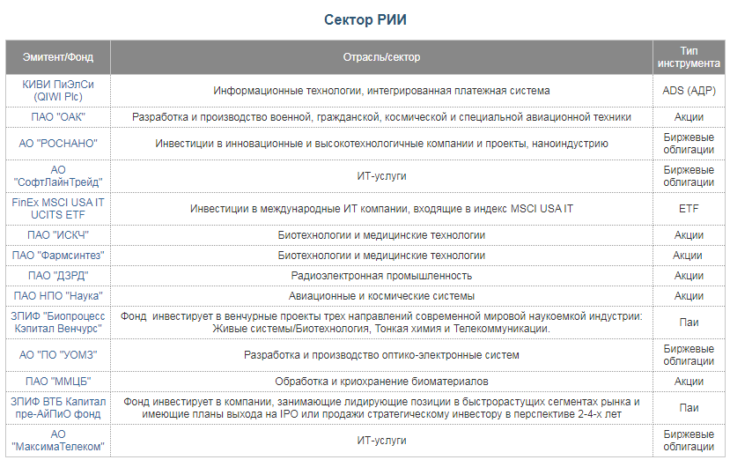

Investing in Securities of High-Tech Companies for One Year

Previously, Russian tax legislation included a special benefit for investments in securities of innovative sector companies. This allowed investors to be exempt from paying NDFL on profits from selling such securities, provided certain conditions were met:

- The benefit applied to stocks, bonds, and shares of closed mutual funds traded on the Market of Innovations and Investments (RII) of the Moscow Exchange;

- The mentioned securities had to be continuously owned by the investor for at least one year;

- Profits from selling such securities were exempt from NDFL without a limit on the income amount;

- The benefit applied to securities purchased between January 1, 2016, and December 31, 2022.

As of now, the program has not been extended. Therefore, this tax benefit can only apply to securities purchased before December 31, 2022, and held by the investor for at least one year. This tax preference no longer applies to new investments.

Purchasing Securities on an Individual Investment Account (IIA)

The Individual Investment Account (IIA) has long been one of the most popular methods for tax optimization for private investors. Previously, investors had access to two types of tax benefits.

IIA Type A – Tax Deduction on Contributions

When making contributions to an individual investment account, investors could receive a 13% tax deduction on the invested amount. The maximum refund was 52,000 rubles per year, corresponding to a contribution of up to 400,000 rubles annually. To qualify for the deduction, the investor needed to have taxable income.

IIA Type B – Tax Deduction on Income

This benefit exempted the investor from paying NDFL on profits from transactions with securities on the individual investment account. No tax was charged when closing the account, provided the holding conditions were met.

For both account types, the minimum IIA existence period was three years.

Since 2024, a new format of the investment account—IIA-3—has been introduced in Russia. New accounts of types A and B are no longer available, but previously opened accounts continue to operate under the previous conditions. New individual investment accounts are only opened under the updated model, which involves a longer investment period and combines elements of the previous types of tax benefits.

Individual investment accounts are opened with brokers and banks operating in the Russian stock market.

Tax Benefits for IIA-3

The new account type effectively combines the advantages of the old IIA-A and IIA-B types but operates with a longer investment period. The tax benefits for IIA-3 are as follows:

Tax Deduction on Contributions

Investors can receive a tax deduction annually on the funds deposited. The deduction amount is 13% of the deposit amount, but not exceeding 52,000 rubles per year (at the standard NDFL rate). If a higher tax rate applies, the refund can reach approximately 60,000–88,000 rubles. The calculation considers deposits up to 400,000 rubles per year.

Exemption of Income from Tax

After meeting the holding period conditions, the investor is exempt from NDFL on investment profits earned on the account. The exemption applies within a limit of 30 million rubles in income over the entire investment period. Dividends on stocks are not included in this benefit and are taxed separately.

Minimum Holding Period

To retain the right to tax benefits, the account must exist for a certain period. The duration depends on the year of opening:

- 2024–2026 — at least 5 years

- 2027 — 6 years

- 2028 — 7 years

- 2029 — 8 years

- 2030 — 9 years

- from 2031 — 10 years

Additionallly, the new regime allows having up to three investment accounts simultaneously if the investor does not have previous IIA types. In other words, IIA-3 retains the tax deduction on contributions (as in IIA-A) and the exemption of investment profits from tax (as in IIA-B), but requires a longer investment period and limits the non-taxable income to 30 million rubles.

Purchasing Coupon-Bearing Bonds

Income from coupon payments for individuals is partially or fully exempt from NDFL under certain conditions:

- Full exemption applies to coupon payments on federal government bonds (OFZ), Ministry of Finance eurobonds, and regional bonds;

- Partial exemption applies to coupon payments on ruble corporate bonds traded on the Moscow Exchange, issued no earlier than January 1, 2017. No tax is due if the coupon yield does not exceed the Central Bank’s key rate by more than 5%. If it exceeds this threshold, NDFL must be paid on the portion of income exceeding the limit.

An updated list of bonds whose coupons are tax-exempt can be found in the ‘Bonds for Individuals’ section on the official website of the Moscow Exchange.

Using Losses to Offset Taxes

The tax payment amount in 2026 can be reduced by losses incurred in previous years. This loss carryforward is possible

FAQ

What is the tax exemption for long-term securities investments?

Investors can be exempt from NDFL on profits from selling securities if they are continuously owned for at least three years, with a maximum tax-free profit of 3 million rubles per full year of ownership.

What are the benefits of an Individual Investment Account (IIA-3)?

IIA-3 offers a tax deduction on contributions (up to 52,000 rubles annually) and exemption from NDFL on investment profits up to 30 million rubles, provided the account is held for a minimum of 5–10 years depending on the opening year.

Are coupon payments on bonds tax-exempt?

Full exemption applies to coupons on federal government bonds and Ministry of Finance eurobonds. Partial exemption may apply to corporate bonds if the coupon yield does not exceed the Central Bank’s key rate by more than 5%.